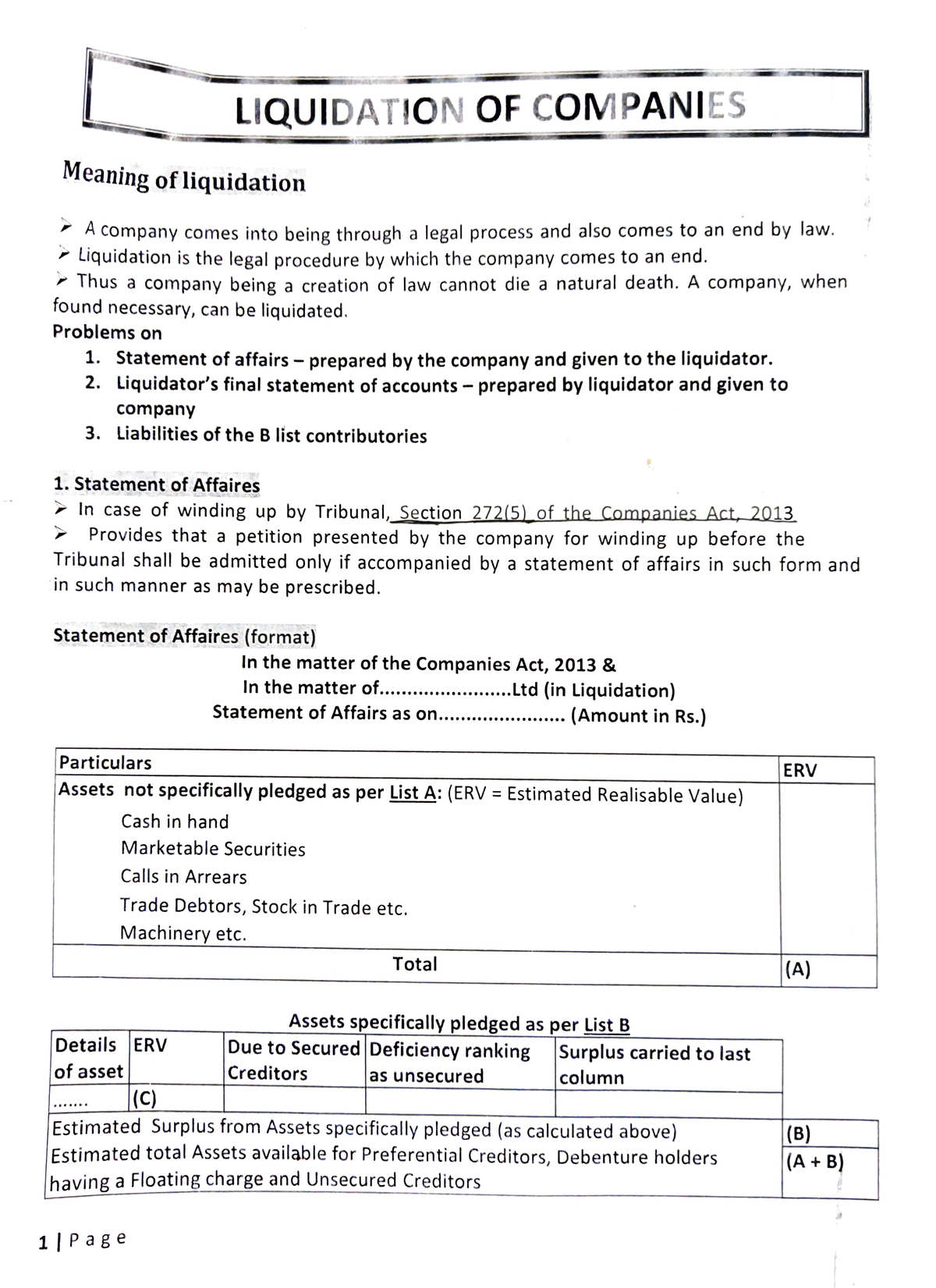

Revelation report

Nigel Stapledon doesn’t work to have, demand, own offers inside or discover money away from any organization otherwise organisation who make the most of this post, and also expose zero relevant associations past its instructional meeting.

Lovers

Having property value set-to feel an option election question, the newest 2022 government funds increases the brand new system the newest Coalition put forward during the 2019 election to simply help very first home buyers.

The initial Home loan Deposit System assists the individuals without the important 20% deposit required by mortgage brokers. For those who meet the requirements, they promises around fifteen% of an effective loan’s really worth, definition consumers normally safer a mortgage which have good 5% put.

On 2021-twenty-two financial 12 months the plan are capped on 10,000 metropolises. The latest 2022 finances is actually broadening that it so you can thirty five,000 per year, as well as a supplementary ten,000 towns and cities to own basic homebuyers when you look at the local portion.

It is going to develop a class to have single moms and dads put when you look at the the new 2021 funds, making it possible for some to go into that have a two% put, raising the limit to 5,000 a-year.

Authorities software to simply help very first home buyers was regularly criticised once the only putting upward pressure to the cost, getting no genuine advantage to first homebuyers. This strategy tend to push-up rates, but not of the same amount just like the property value the fresh advice.

What exactly is riding right up possessions pricing

Australia’s relatively high housing prices is also usually feel attributed to the significant income tax advantages of assets possession and you will rigidities into supply front side, such as for instance zoning and other regulating restrictions.

In the past a couple of years this type of activities was supplemented because of the the fresh new potent mixture of COVID-19 and you will low interest.

The functional-from-household revolution created a surge sought after having huge houses and you will a bad credit personal loans Georgia change to help you outlying and you will local areas at the same time because central financial institutions pushed formal rates close to no to trigger a failure economic climates.

An extra-best bet

The newest deposit ensure program strategy to help first homebuyers try what economists call one minute-best option. A finest provider do significantly more in person address the consult and provide grounds operating up prices. In the place of this, brand new government’s plan is to try to promote basic-home buyers an enhance over someone else.

It can push-up pricing, however by exact same matter just like the worth of the newest financing guarantees. To do that all people would need to have the same concession, and there must be no influence on the supply out of homes. Have regarding housing market could be slow to reply but it does transform that have demand.

Over the past 2 yrs basic home buyers have made right up regarding 20% of the many consumers. So it program, even after the newest expanded cap, may benefit less than half that count on the 7% of all customers.

So the strategy are certain to get specific influence on possessions costs, although not sufficient to offset the worth of the support to the individuals people just who meet the requirements. At the same time, those trading homes will pay marginally so much more. Very commonly dealers, and you will renters inside owed course.

Deeper control, greater risk

The big anxiety about so it scheme ‘s the exposure those playing with they purchasing a property are able to get into monetary difficulties and default on the financial.

This is a contributing factor in the united states subprime financial crisis one contributed to the worldwide economic crisis from 2007-08. Guidelines designed to rating reduced-income domiciles towards the markets seemed to works before crisis strike. Next domestic pricing tumbled and some was basically compelled to promote at the large losses.

Once you control upwards, borrowing from the bank 95% otherwise 98% of one’s worth of a home, youre much more started if the rates slip. Actually a little decline could over eliminate the security.

Houses is not chance-100 % free. Time matters. Household pricing can slide in addition to go up. With rates growing, and you can grand internationally economic suspicion, certain negative outcomes from this strategy along the song can’t be eliminated.